From 1 January 2026, the Carbon Border Adjustment Mechanism (MACF) is entering its implementation phase.

I thought like one of the pivotal instruments of European Green Deal, it marks a significant break in the Union's climate policy. For the first time, a carbon price is being applied to imports, in order to re-establish fair competition between European and non-European producers.

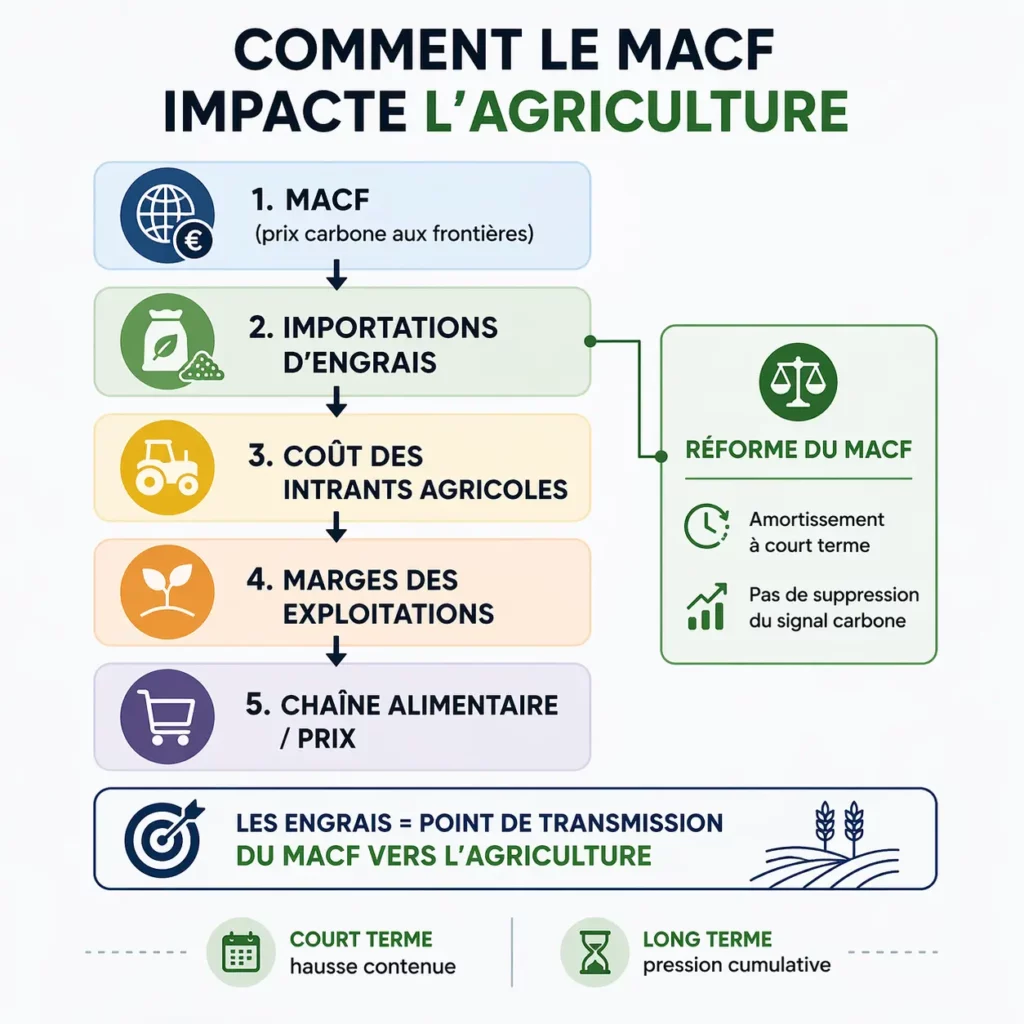

Behind this objective, the entry into force of the MACF reveals a more complex reality, with differentiated effects depending on the sectors. Among them, the Nitrogenous fertilisers occupy a unique position: simultaneously high emitters, essential for agriculture, and massively imported, they crystallise a large part of the economic and political tensions linked to the system.

A climate adjustment mechanism based on the alignment of carbon prices

Until now, European climate policy has been based on a structural imbalance. European producers were subject to a carbon price via the ETS market (Emissions Trading Schemes – or EU Emissions Trading System, EU ETS), while imported products entered the domestic market without equivalent constraints. This asymmetry fuelled a Double risk : loss of industrial competitiveness and carbon leaks, that is to say, the relocation of production to countries with less demanding climate requirements.

The MACF aims to correct this situation, by charging imports a carbon price equivalent to that borne by European industries. Concretely, from 2026, importers of certain products will have to acquire CBAM certificates, the price of which is indexed to that of ETS carbon quotas.

The implementation of the mechanism was done in two stages:

- Between October 2023 and December 2025, the transitional phase imposed a reporting obligation on companies, without actual payment. This period allowed for testing calculation methods, identifying data collection difficulties, and measuring the risks of evasion.

- From January 2026, the MACF will fully come into effect.

It initially applies to six sectors (steel, aluminium, cement, fertilisers, electricity and hydrogen) which alone account for nearly half of European industrial emissions.

The final cost depends on several parameters:

- the carbon price on the ETS market (around €70 to €90/tCO₂ in 2025),

- the actual carbon intensity of the imported product, the level of free allowances still granted to European industries (which are set to be phased out by 2034)

- and, where applicable, the existence of a carbon pricing mechanism in the exporting country.

In the absence of reliable data provided by the exporter, the importer must apply default values, which are generally more penalising.

Why fertilisers are a separate case for the MACF

Nitrogenous fertilisers are among the sectors covered by the MACF, but their situation differs profoundly from that of other industrial products.

Fertilisers represent 6 to 12% of agricultural input costs, and the European Union is heavily reliant on imports: 30% of the nitrogen consumed is imported. France, the leading European user, is Net importer, with nearly 4.8 million tonnes imported for only 0.5 million tonnes exported.

From a climate perspective, fertilisers are also a sensitive sector. Their production and use in the field generate significant emissions of CO2 and N2O, a gas with Very high heating power. Globally, nitrogen fertilisers account for 5 % greenhouse gas emissions.

But this carbon intensity must not mask another reality: the European fertiliser industry is already fragile. Very dependent on natural gas (of which the EU imports nearly 80 %), it has been particularly affected by the Soaring energy prices since 2021. In many cases, European units are less carbon-intensive than their non-European counterparts, but are more exposed to production costs. In this context, the strict application of the MACF would risk causing an immediate economic shock, with knock-on effects on agriculture.

Any increase in the price of fertilisers is directly reflected in agricultural holdings, which are already facing high market volatility and squeezed profit margins. It is this direct downstream impact of carbon taxes that makes fertilisers economically and politically sensitive.

A reform to secure the entry into force of the Carbon Border Adjustment Mechanism

Following this initial transitional phase, the MACF was substantially reformed to be more easily implemented.

- On the one hand, this reform reinforce clearly the mechanism, in widening the scope to certain new products, in order to limit workarounds through partial outsourcing of production.

- On the other hand, the Commission complements the system with mechanisms for managing the short-term effects of the MFF on the most exposed sectors. The temporary decarbonisation fund, financed by 25% of MACF revenue, helps to mitigate the loss of competitiveness by making support conditional on measurable decarbonisation efforts. The challenge is to avoid a too-brutal carbon shock producing counter-productive effects (relocations, loss of industrial capacity, downstream tensions) which would weaken both the climate ambition and the viability of the system.

The differentiated treatment of fertilisers within the framework of the MACF

Within this framework, Fertilisers benefit from a specific scheme, and will be taxed at a lower rate than other sectors. Whilst other sectors will face an increase of 10 % from 2026, followed by 20 % in 2027 and 30 % in 2028, the rate applied to nitrogen fertilisers will be capped at 1 % in 2026, with a more gradual increase thereafter.

This would cap the rise in fertiliser prices at 7 % as soon as the MACF comes into force (this figure represents an average estimate, calculated across the entire European market).

Concretely, this so-called «net» increase is the result of a combination of several factors:

- The uplift applied is heavily capped for fertilisers, which reduces the theoretical carbon cost borne by imports.

- European producers continue to benefit, at least temporarily, from free quotas within the framework of the European carbon market, which mitigates the increase in production costs.

- The Commission assumes that the additional cost generated by The MACF will not be supported by a single actor, but distributed throughout the value chain.Between fertiliser producers, importers, intermediaries and end-users.

In this context, the figure of 7.1% for Q3 should be understood as a estimation, resting on economic assumptions.

For agriculture, this rise, even if limited, remains significant. In a context of already squeezed margins and agricultural prices largely determined by international markets, any increase in the cost of inputs acts as an additional constraint. The main risk for farms therefore lies not in an immediate shock but in a cumulative effect.

Rethinking the agricultural transition beyond price, the mission of Carbone Farmers

For solution, the debate surrounding the MACF and fertilisers highlights the limitations of climate policies based solely on prices.

A central question is also that of reducing reliance on mineral fertilisers, by opting for a more systemic agronomic approach cultural-livestock integration, crop rotation diversification, legume valorisation, optimised mineral fertiliser management and organic fertiliser valorisation.

In this context, agricultural carbon schemes can play a key role, not as simple compensation, but as a lever for economic reallocation, enabling farms to regain the necessary room for manoeuvre in the face of various regulatory and energy shocks.