The 30 January 2026, the GHG Protocol published on the Land Sector and Removals Standard (LCRS). This new standard governs the accounting of agricultural emissions, land use change (LUC), and CO₂ sequestration in corporate climate inventories. It will come into effect on 1 January 2027. A Technical guide detailed will be published at second quarter 2026. The current text guides corporate climate reporting and how to integrate carbon sequestration and land-related emissions.

This article offers a structured breakdown of the GHG Protocol, the new LSR standard, and its implications for agricultural value chain businesses.

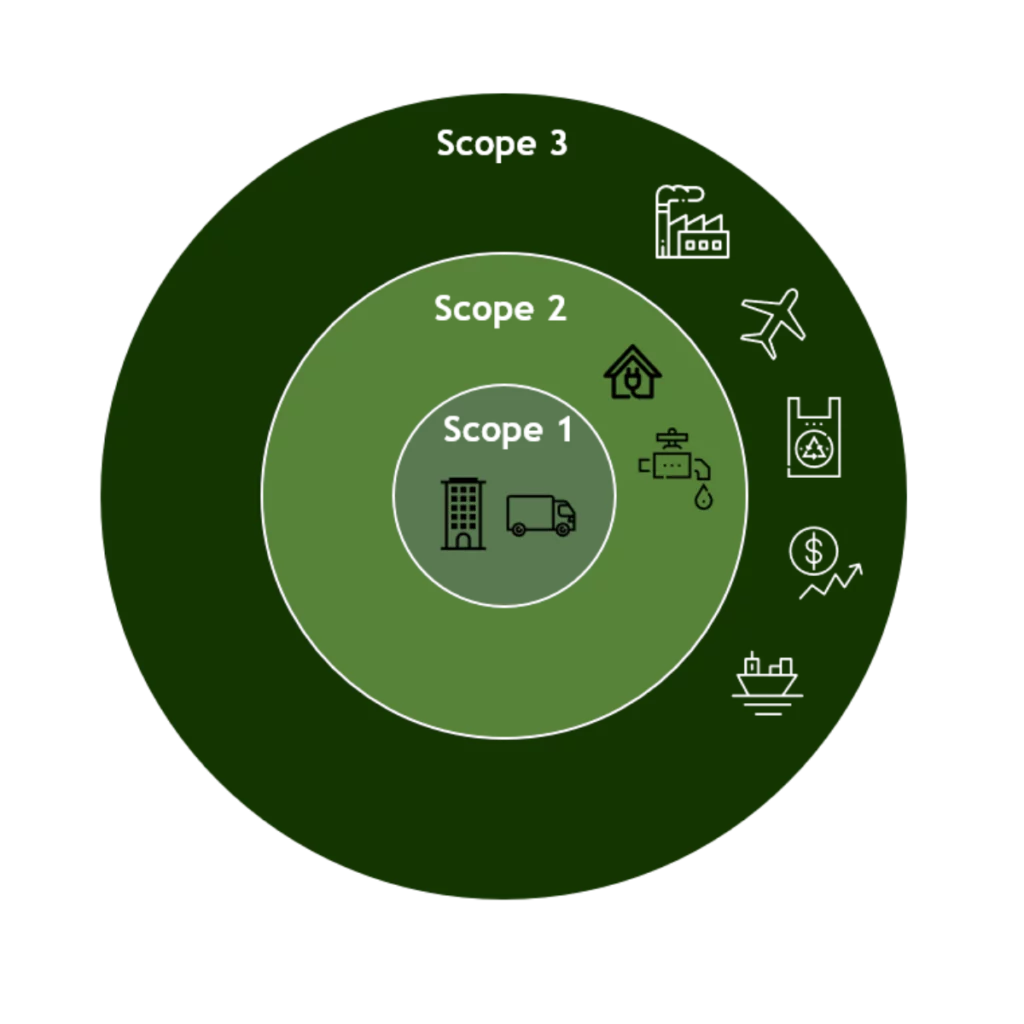

The GHG Protocol: A Cross-Cutting Methodological Framework

Le GHG Protocol est un standard international ouvert pour la comptabilisation et le reporting des émissions de gaz à effet de serre (GES). Il fournit des directives détaillées pour les entreprises et les organisations afin de mesurer et de gérer leur empreinte carbone. Le GHG Protocol classe les émissions en trois catégories principales : les émissions de portée 1 (directes), les émissions de portée 2 (indirectes liées à l'énergie) et les émissions de portée 3 (autres émissions indirectes). Methodological framework developed by the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD). It is now the global benchmark for accounting for greenhouse gas (GHG) emissions.

It structures companies' carbon accounting around three scopes:

- Scope 1: Direct emissions

- Scope 2: Emissions from purchased energy

- Scope 3: Indirect value chain emissions

Furthermore, this framework serves as the basis for most International climate regulations and frameworks, whose directive CSRD (Corporate Sustainability Reporting Directive) and the SBTi (Science Based Targets initiative). The GHG Protocol operates by Thematic standards. The Corporate Standard and the Scope 3 Standard were the main texts used until now. The land sector remained partially covered. No dedicated standard governed agricultural practices, carbon sequestration in soils, and LUC. The LSRS therefore fills this void.

Why a specific standard for the land sector?

Agriculture and land-use change account for approximately a quarter of global GHG emissions. Agri-businesses are concerned by these emissions via their Scope 3 Their agricultural value chain.

Up until now, accounting has been based on:

- statistical approximations

- heterogeneous methodologies

- partial storage integration

The LSRS therefore introduces a more precise architecture and requires accounting for:

- Land use change (LUC) emissions

- land management emissions

- biogenic emissions

- The risks of emissions leakage

It also frames the optional integration of carbon storage into the inventory.

Permanence: a recommendation now fully integrated into the LSRS

Within the framework of the LSRS, the accounting for removals is based on a tracking over time. The carbon sinks are linked to a Stock, which can evolve according to agricultural practices, natural conditions, or changes in land use.

This requires businesses to be able to to follow these developments over time, particularly when:

- The parcel tracking has been interrupted

- the link to the supply areas is uncertain

- storage practices are not being maintained

So, stock must be monitored, in addition to being recorded at an initial point in time. A negative variation in stock can thus lead to an adjustment of the removals already accounted for.

End of book-and-claim for inventories

The LSRS introduces the fact that’A tonne integrated into a GHG inventory must be linked to a traceable physical flow. in the company's value chain.

The book-and-claim model« rests on a Disassociation between the physical product and the environmental attribute. A company can purchase a “low-carbon” certificate or attribute associated with agricultural production without physically receiving that production: in this case, The trade flow and the environmental flow are decoupled.

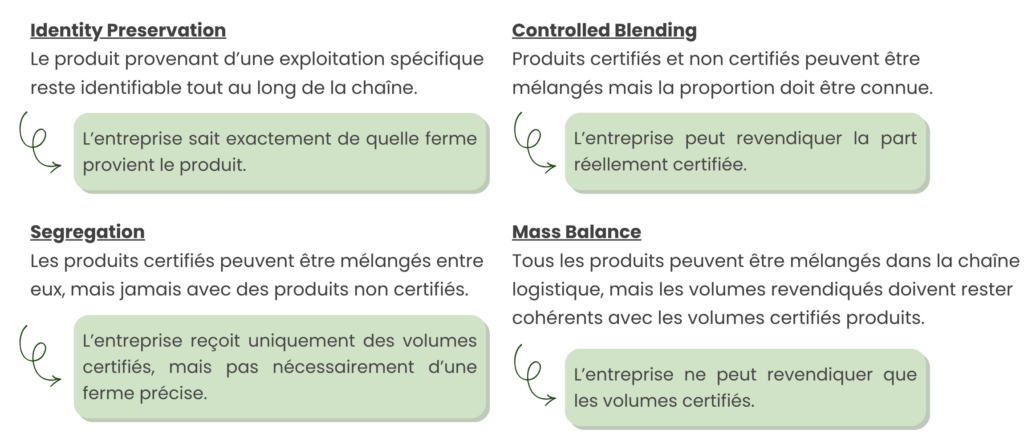

Consequently, the LSRS explicitly excludes book-and-claim when it comes to incorporating agricultural emissions or removals into Scope 1 or Scope 3 inventory. The standard prioritises chain of custody models instead which maintain a physical link between production and purchasing.

- TheIdentity Preservation implying that the product remains identifiable throughout the chain. A batch can be linked to a defined farm or group of farms.

- The Segregation allows the mixing of certified products with each other, but excludes mixing with uncertified streams. The stream remains contained within a controlled perimeter.

- The Controlled Blending allows a certified / non-certified mix provided that the proportion is precisely known and documented. The claim is proportional to the volume actually covered.

- The Mass Balance Does not track each batch individually. It ensures consistency between volumes received and volumes claimed over a defined period and scope. The LSRS authorises Mass Balance but strictly limits its use. The geographical scope must be clearly defined. Volume reconciliations must be carried out over a limited period. Multi-region aggregations without justification are excluded.

These restrictions aim to prevent geographical dilution. The wider the perimeter, the more fragile the link between a declared tonne and a biophysical reality. The standard also imposes a coherence of spatial boundaries. A company cannot define a broad scope for its emissions and a narrow scope for its removals: the rules must be applied symmetrically.

In summary, this evolution frames the reporting of companies in the agricultural value chain, which must apply to connect the data, physical volumes and supply flows to integrate tonnes of CO₂e into their reporting.

This is precisely the type of structuring that tools like FarmGate Metrics permit. Our platform is designed to certify environmental indicators (including the Product Carbon Footprint) and secure sustainable production volumes. Our tool also allows for the generation of ISO 14067 certified attestations, which can be transmitted to all supply chains.

Carbon credits: reinforced requirement for separation of uses

The LSRS is introducing a rule for carbon credits generated on land that falls within a company's Scope 3: The same tonne of CO₂e cannot be used twice in the inventory.

In certain current arrangements, a company can support an agricultural project that generates carbon credits, while also incorporating the emission reductions or removals associated with these same practices into its Scope 3. It then benefits from both a «inventory" effect »and of a «credit' effect ».

From now on, if an operation located within a company's Scope 3 generates carbon credits, the tonnes associated with these credits must be deducted from the inventory. This requires being able to explicitly distinguish the uses of tonnes, which necessitates systems capable of ensuring fine-grained traceability at the farm level.

The LSRS also imposes a duty of transparency. Any area within Scope 3 that generates credits must be identified and reported. This requirement may apply even if the commodity produced by the operation is not directly purchased by the company. The determining criterion is the presence within the spatial boundary.

Land Use Change (LUC): enhanced requirements and the end of approximations

The LSRS significantly tightens the treatment of changes in land use. This latter corresponds to emissions generated when a natural ecosystem is converted to agricultural land (deforestation, conversion of grasslands, etc.). These conversions release the carbon stored in biomass and soils. These emissions can be significant and spread over several years.

In many current inventories, this LUC is handled using national or regional statistical data. The company applies an average emission factor associated with a country or a commodity.

The LSRS specifies that the calculation of the LUC must be carried out at the level of the Land Management Unit (LMU). This corresponds to the land management unit, generally on the scale of the farm or a defined agricultural perimeter. The objective is to bring the calculation closer to the biophysical reality.

The standard also requires an evaluation period covering the 20 years preceding the reporting year (at a minimum). In other words, the company must examine whether an ecosystem conversion has occurred in the last twenty years on the land concerned. This timeframe aims to capture deferred effects from a past conversion. The depreciation profile used is not an equal split over twenty years; it follows a Linear decreasing scheme. This means that a recent conversion carries more weight in the inventory than an older conversion.

The LSRS also imposes a Methodological consistency over time. If the company changes its method for calculating the LUC, it must recalculate its baseline to ensure data comparability from one year to the next.

In short, this should strengthen the need for precise mapping of supply areas and the importance of tools capable of linking a farm, its history of land use, and the volumes actually purchased.

Leakage: explicit recognition of indirect risk

Leakage or the risk of emissions displacement

The LSRS introduces a new and structuring requirement: the consideration of emissions displacement risk, or «leakage».

An action taken within a value chain can reduce emissions in a given scope while displacing them elsewhere. If a company changes its procurement practices or supports certain agricultural practices, this can affect global food production. However, as global agricultural land is finite, this implies pressure on land. Leakage corresponds to this displacement dynamic. For example, if a company supports the conversion of agricultural land to non-food production, such as biofuels, the corresponding food production will potentially be shifted to another region.

This new production may lead to the conversion of natural ecosystems elsewhere. The overall result may be neutral, or even negative, despite an apparent improvement within the company's direct scope.

Identifying high-risk activities for leakage

The LSRS explicitly identifies certain high-risk-of-leakage activities. These include:

- The Foodstuffs for non-food uses,

- The food production cuts linked to a change in land use,

- The yield reductions linked to certain farming practices.

The standard requires companies to identify and assess this risk when they are exposed to these situations. Leakage is not directly incorporated into the physical Scope 1 or Scope 3 inventory: it must be reported separately as it corresponds to indirect emissions located outside the company's physical boundary.

However, the standard remains largely prescriptive about the exact method of evaluation. It requires identification and transparency, but leaves room for interpretation regarding the tools to be used.

Carbon opportunity cost

Finally, the LSRS also introduces the notion of «carbon opportunity cost » (COC), which is in a way the unit of measurement for leakage. This concept refers to the carbon cost associated with the use of land for a given activity rather than the preservation or restoration of a natural ecosystem. In other words, land used for a given production represents a missed opportunity for natural carbon storage.

What this means for agricultural and agri-food businesses

Until now, many companies have been able to manage their agricultural emissions mainly from average emission factors and statistical models. Now, the LSRS requires them to be more accurate and consistent in their climate reporting. In short, these changes concern:

- The data Generic data will progressively become insufficient if more specific data is available. The ability to mobilise data at the farm or supply basin level is a differentiating factor.

- Traceability Models based solely on regional attributes or averages can no longer incorporate certain tonnes into the inventory. Companies must link purchased volumes, supply areas, and agricultural practices.

- Tracking over time Permanence introduces a responsibility over time. Integrated offsetting today can generate a future reporting obligation in the event of stock loss, thus embedding a company’s carbon strategy in the long term.

- Strategic coherence Companies must clarify the use of carbon credits. A tonne cannot be used simultaneously to generate a credit and improve Scope 3 inventory.

- Le LUC and leakage there is increasing pressure for a more granular analysis of indirect impacts and land use trade-offs.

In short, the LSRS mandates a clear change: agricultural carbon accounting must now be based on traceable data, linked to physical flows and monitored over time. This makes tools essential for connecting farming practices, plots, volumes and climate reporting across value chains.

Carbone Farmers meets these requirements with FarmGate Metrics, certified to ISO 14067, which allows a shift from reporting based on averages to management based on on-the-ground data, directly usable by value chains.